- 10 Lenders Said No. SmartLend Found the One Who Said Yes — in 3 Days.

- Singapore SME Grants 2023–2026: What Actually Changed (And What Nobody Tells You)

- Why SME Loan Approval Rates Dropped to 70% — And What the Iran War Means for 2026

- Real CBS Makeovers: 3 Case Studies of SME Owners Who Turned Bad Credit Around

- Ask SmartLend: Why Did My SME Loan Get Rejected?

- Introducing SmartLend Concierge: A Helping Hand for SME Loans

- Legal Ways to Lighten Your Company’s Tax Burden in Singapore

- A Wake-Up Call on Director Duties: The Envy Saga and Other Cautionary Tales in Singapore

- Surviving Cash Flow Crunch: How SMEs Can Use Short-Term Financing Wisely

- Unmasking Business Loan Fraud: How Syndicates and Rogue Brokers Game Singapore’s Lending System—and How AI Can Stop Them

Corporate Income Tax Filing Season 2023: 6 Things SMEs Need To Know

The article was published on 16 Oct 2020 and was most recently updated on 27 Oct 2023

The Corporate Income Tax filing season for the Year of Assessment (YA) 2023 is here again, so please take note that the filing deadline is 30th November 2023. E-filing is compulsory and paper filing will no longer be accepted.

Time to tidy up your accounts and prepare the relevant documents for your accountant!

As long as the control and management of your business is exercised in Singapore, your company will be considered a tax resident in Singapore, and here are 6 things you need to take note of when filing your taxes.

1. Corporate Tax Rate

As one of the leading financial hubs in the world, Singapore’s corporate income tax rate has also been one of the lowest in the world. This has made Singapore an attractive investment destination and an advantage for incorporating a company in Singapore.

Since 2010, the corporate income tax rate has been fixed at 17% regardless of whether it is a local or foreign company. This is calculated based on the company’s chargeable income, which is the taxable income less allowable expenses and other allowances.

The effective tax rate is further reduced with the various tax relief schemes and rebates available.

2. Tax Exemptions for companies

In Singapore, there are tax reliefs to help reduce companies’ tax, such as the Tax Exemption Scheme for new start-up companies and Partial Tax Exemption for all companies.

Introduced in YA 2005 to support entrepreneurship and grow local enterprises, new start-up companies are given the following tax exemption for their first three consecutive YAs:

- YA 2020 onwards: 75% exemption on the first S$100,000 of normal chargeable income; and a further 50% tax exemption on the next S$100,000 of normal chargeable income.

- YA 2019 and before: Full exemption on the first S$100,000 of normal chargeable income; and a further 50% exemption on the next S$200,000 of normal chargeable income.

To qualify for tax exemption for new start-ups, eligible companies must satisfy these three qualifying conditions:

- The company must be incorporated in Singapore;

- The company must be a tax resident in Singapore for that YA;

- The company’s total share capital is beneficially held directly by no more than 20 shareholders throughout the basis period for that YA where:

- all of the shareholders are individuals; or

- at least one shareholder is an individual holding at least 10% of the issued ordinary shares of the company.

The Tax Exemption Scheme for new start-up companies is for the first three consecutive YAs, whereby the first YA depends on the financial year end chosen and the closing date of the first set of accounts. This is the basis period during which the company is incorporated.

From the 4th YA onwards, new start-up companies can still can enjoy the Partial Tax Exemption like all other qualifying companies:

- YA 2020 onwards: 75% exemption on the first S$10,000 of normal chargeable income; and a further 50% tax exemption on the next S$190,000 of normal chargeable income.

- YA 2019 and before: 75% tax exemption on the first S$10,000 of normal chargeable income; and a further 50% tax exemption on the next S$290,000 of normal chargeable income.

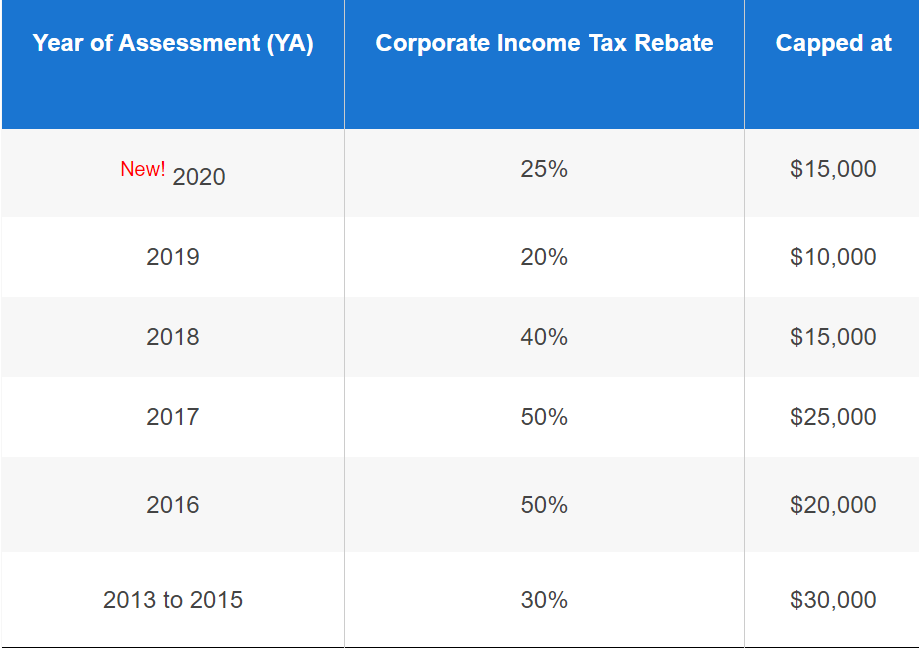

3. Corporate Income Tax rebates available for all companies

Corporate income tax rebate is given to all companies and helps to ease business costs. This is applicable for YAs 2013 to 2020 and is computed on the tax payable after deducting tax set-offs (e.g. foreign tax credit).

In 2020, the Government announced that all companies will be entitled to a 25% corporate income tax rebate, subject to an annual cap of S$15,000.

Companies do not need to factor in the rebate when filing the Estimated Chargeable Income (ECI) as IRAS will compute it and allow the rebate automatically.

Source: IRAS

4. Simplified Corporate Income Tax Form

Filing of taxes has always been a hassle for companies.

Earlier in July 2020, a new simplified Corporate Income Tax (CIT) Return form was implemented to make it easier and faster for Small and Medium Enterprises (SMEs) to file their corporate taxes.

Companies with straightforward tax matters are able to file taxes by filling out as few as six essential fields, including revenue and net profit or loss, through the simplified version of the standard CIT Return Form C-S, also known as Form C-S (Lite).

The qualifying conditions to e-file Form C-S are:

- The company must be incorporated in Singapore;

- The company must have an annual revenue of $5 million or below

- The company only derives income taxable at the prevailing corporate tax rate of 17%; and

- The company is not claiming any of the following in the YA:

- Carry-back of Current Year Capital Allowances/ Losses

- Group Relief

- Investment Allowance

- Foreign Tax Credit and Tax Deducted at Source

Hence, Form C-S (Lite) allows companies that fulfil the above criteria but has annual revenue of S$200,000 or less to be able to file taxes easier. This is expected to benefit about 60,000 SMEs that fulfil the current criteria to e-file Form C-S.

If your Singapore company is unable to use Form C-S or Form C-S Lite, you should file Form C for your tax return. Make sure to include your audited or unaudited financial statements, tax computation, and any other required documents.

Remember to submit Form C, Form C-S, or Form C-S Lite even if your company is not making a profit or is experiencing a loss.

5. How to File Form C-S (Lite)

- Prepare your company’s tax computation and supporting schedules.

You can refer to IRAS website on Preparing a Tax Computation and Basic Corporate Tax Calculator for information on how to prepare the company's tax computation.

Companies are not required to submit their financial statements and tax computations, but should have them ready in the event that the Inland Revenue Authority of Singapore (IRAS) calls for them.

- Check that your company fulfils the following requirements:

- Company is incorporated in Singapore;

- Annual revenue of S$200,000 or below;

- Your company only derives income taxable at the prevailing corporate tax rate of 17%; and

- You are not claiming any of the following: Carry-back of current year capital allowances / losses, group relief, investment allowance and foreign tax credit and tax deducted at source

Otherwise, refer to IRAS if your company should file Form C-S or Form C

- To be able to e-file Form C-S (Lite), company staff or tax agents have to be authorised for ‘Corporate Tax (Filing and Applications)” in CorpPass.

Next, login via mytax.iras.gov.sg, you will be presented with the option to select Form C-S (Lite) when you input the companies' revenue to be $200,000 or below under Form C-S at the "Form Type Selection".

Source: IRAS

You can also refer to the step-by-step guide on how to e-file your company’s Form C-S (Lite).

Step 3b")

6. Digital Solutions for Tax-Related Processes

In line with Singapore’s Go Digital movement, IRAS has also implemented more digital solutions to enhance the taxpaying experience for companies.

Companies now have the convenience to pay their corporate taxes via PayNow QR, which provides instant settlement and real-time updates of any outstanding tax balances. From mid-2021 onwards, PayNow Corporate will also be available for companies that link their Unique Entity Number (UEN) to their corporate bank account to receive CIT refunds within seven days from the credit arising.

Furthermore, the preparation and filing of company’s statutory returns can be automated by using specified accounting software linked to systems of IRAS and the Accounting and Corporate Regulatory Authority (ACRA). In August, IRAS and ACRA partnered with five software companies to incorporate statutory filing requirements into accounting software to facilitate the automation of tax computation and to file CIT returns directly to IRAS and Annual Returns for Financial Statements directly to ACRA.

The software that currently offer it are Netiquette O2O Business Suite and SME Cloud Exchange Network. The solution will be made available progressively in AutoCount Accounting, Deskera ERP and Realtimme Cloud Solutions. This solution is expected to benefit 200,000 SMEs with annual revenue of S$5 million and below. Companies can utilise the Productivity Solutions Grant, Start Digital Pack or the Digital Resilience Bonus to fund the adoption of the enhanced accounting software.

Last but not least, paper notices will soon be phased out. Companies are required to update their email address to receive e-notifications from IRAS via the e-service “Update Notice Preferences” in myTax Portal from January 2021.

Read also: Singapore Income Tax: Filing Employee Earnings

Read also: You've Heard It Before: Charitable Donations Can Help Your Business With Your Taxes. But How?

Read also: Should Companies Voluntarily Register For GST?

-------------------------------------------------------------------------------------------------------

Got a Question?

WhatsApp Us, Our Friendly Team will get back to you asap :)

Share with us your thoughts by leaving a comment below!

Stay updated with the latest business news and help one another become Smarter Towkays. Subscribe to our Newsletter now!

_940.png)